How was "Compensation Poker" 2U?

Post Earnings Wrap-Up and Discussion of 2U, Inc. (TWOU)

Welcome to the Nongaap Newsletter! I’m Mike, an ex-activist investor, who writes about tech, corporate governance, the power & friction of incentives, strategy, board dynamics, and the occasional activist fight.

If you’re reading this but haven’t subscribed, I hope you consider joining me on this journey.

Last week’s newsletter covered curious changes to 2U, Inc.’s (TWOU) equity compensation prior to Q4 2019 earnings, and I openly pondered the materiality of these changes to TWOU shareholders:

There’s a game of “compensation poker” happening right now where you get to decide if the Company’s most recent equity grant to management is a material “tell”.

With the Company announcing consensus-beating Q4 2019 earnings and guidance, I think it’s fair to say the changes were a material “tell”.

Primary Post-Earnings Takeaway: If you don’t read anything else, I believe Compensation Committee Chair Jack Larson has no business being on this Board and shareholders should push for him to step down. Incidentally, he is also up for re-election in the upcoming 2020 annual meeting.

For this newsletter, I’m going to:

Share my post-earnings thoughts and key takeaways

Speculate on “what’s next?”

Activate Substack comments! I’d love to hear your thoughts and learnings.

How was TWOU’s “compensation poker” to you?

This was a “real time” situation for all of us so I’d love to hear your thoughts and how you approached the situation after reading last week’s newsletter. Don’t be shy and leave a comment!

Thank You

A quick thank you to everyone who signed up to my premium newsletter. A week into my new adventure and I’m incredibly surprised and grateful at the response. I appreciate your vote of confidence and am working on a few premium pieces that I hope to share with you soon.

Corporate Governance “Dark Arts”

When I started writing about Corporate Governance “Dark Arts”, I told you my primary goal was to teach “good” corporate governance by showing how insiders profit from “bad” governance practices, especially “spring loading” equity.

As I’ve said many times before, if you can correctly read the situation and recognize a material “spring load” is happening, you can trade alongside management’s greed.

Note: I don’t endorse YOLO options trading strategies.

TWOU is the first time I’ve publicly written about a potential “spring load” situation as it was happening and am shocked at how well the story played out.

TWOU turned into a perfect “dark arts” case study.

YOLO at TWOU

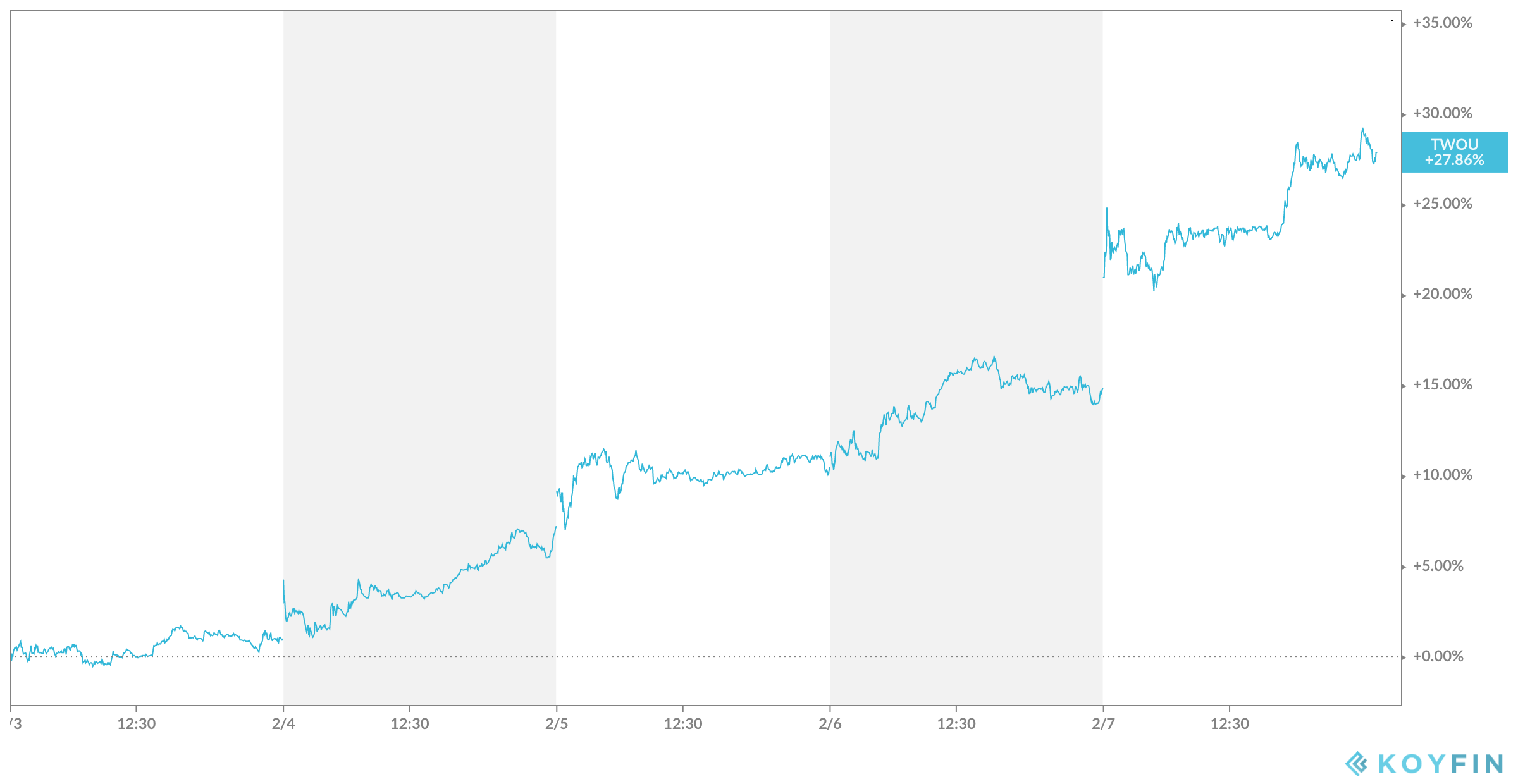

Speaking of YOLO, it definitely felt like a bunch of folks decided to go YOLO on TWOU. I was honestly surprised at how much the stock steadily ran BEFORE earnings. I’m not taking credit for this move. It’s more of a curious observation.

Overall, I hope this past week has shown you that if you can blend an understanding of corporate governance, fundamentals, and human behavior ("read the man, not the cards"), there are opportunities for outsized returns. I think most folks are comfortable throwing in a flyer position if they nail 1 or 2 out of 3, but if you can nail 3 out of 3 there’s an opportunity to invest with size. (Not investment advice, just a perspective.)

Post-Earnings Thoughts and Key Takeaways

“In the second half of 2019, we focused the sales process on aligning faculty members with specific courses. I am pleased to tell you that for 2020, we’ve already slotted 90% of our planned new courses. Nearly the entire year is slotted. What a difference six months makes. I am proud of our team for this turnaround.”

- CEO Christopher Paucek (Q4 2019 Earnings)

After a stock blows up, I like to listen to the earnings call (usually the next 2-3 quarterly calls). I’ll read the transcript afterwards, but I want to hear the tone of the CEO since these calls are usually incredibly important check-ins with shareholders.

Is management energized? Excitable? Do they sound like they believe in the turnaround plan? Do they have confidence in the plan as sell-side prods them and asks follow-up questions?

After listening to the TWOU call, it seemed pretty clear that the CEO Christopher Paucek was hyped (for lack of better description). Now I know this could be his general personality, but you could hear his belief that the turnaround plan was underway. (I acknowledge this emotion check could be “fool’s gold”so definitely do your own homework.)

While the Compensation Committee (led by Chairman Jack Larson) sets the grant timing, it’s pretty clear from that call that the CEO would be pretty open and enthusiastic about getting equity before earnings given his bullish tone on the call.

Other post-earnings thoughts and key takeaways:

Anecdotally, TWOU’s stock run (25% to 30%) is within the range of “spring load” outcomes I’ve seen. It’s probably on the high-end but nothing that makes me go “wow, this is crazy”.

I didn’t discuss this in the previous newsletter since it occurred after I posted, but I thought it was peculiar TWOU announced they were expanding their partnership with London School of Economics (a bullish, potentially market expanding announcement) after management received their grants. Management teams have a lot of control over the timing of releasing information and I thought it was interesting the announcement occurred the way it did.

Management confirmed my speculation that they replaced stock options with performance shares. I don’t know what the metrics/hurdles are so please share them in the comments if you know them.

Stock based compensation for 2020 was guided to be $80 million (up from ~$52 million in 2019 and $31 million in 2018) driven by usage of performance shares, changing the vesting schedule to 3 years instead of 4 years to match “market” practice, and a higher number of plan participants.

I seriously question the ramp in stock based compensation (is it to manage cash flow issues?), and since they called out “market” practice to justify changes to the vesting schedule I wonder why TWOU also didn’t follow best practice of granting equity after earnings.

Overall, the more I think about it, I would not dismiss the notion that the Compensation Committee used the most recent grants as a pseudo “makeup grant” to offset the underwater options CEO and management team received in prior years.

What’s Next?

This is not investment advice, but I’d be careful and stay vigilant when it comes to holding stock of companies that practice “spring loading”. Their willingness to cut corners and not do things the right way eventually bites them in the long run.

Also, be careful relying on an activist to push the stock up further. When the stock runs as much as TWOU has, there’s disincentive to push the agenda. The Director nomination window is approaching so I wouldn’t completely dismiss the possibility of a negotiation and settlement.

A part of me even thinks the Board pushed equity grants early to get compensation out of the way before potentially settling with an activist and giving them seats on the Board.

Regardless of activist involvement, I believe Compensation Committee Chair Jack Larson has no business being on this Board and shareholders should push for him to step down. Incidentally, he is also up for re-election in the 2020 annual meeting.

Finally, even if an M&A transaction is on the table, there’s no guarantee a deal will occur or that a deal will occur at a premium that shareholders will approve.

The Gambler

That’s all I got for now.

“Compensation Poker” is one of the more interesting “games” in the market, but you must be thoughtful in your approach and do your homework. As Kenny Rogers would sing in The Gambler:

You've got to know when to hold 'em

Know when to fold 'em

Know when to walk away

And know when to run

You never count your money

When you're sittin' at the table

There'll be time enough for countin'

When the dealin's done

See you at the next newsletter!

left a comment because overlord told me 2

Did you conduct any fundamental analysis of the equity along with this analysis? Do you agree with the work of Citron (https://citronresearch.com/twou-for-profit-education-with-an-f-in-investability/) or is this outside of that?