Illumina: Unidentified Financing Operation?

Exploring the mysteries of the Milky Way (Investments Group), Helix, and beyond

Summary: This write-up is probably the governance equivalent of sharing “proof” that UFOs might actually be real and there’s a conspiracy to hide it from the public.

The “UFO” in question is Milky Way Investments Group and the “conspiracy” centers around their $125 million investment in Grail’s $390 million Series D round.

The mosaic of disclosures seem to infer that Milky Way was potentially used to “lock in” gains on undisclosed shares held by early holders (i.e. Illumina insiders) of Grail shares/economic interest acquired through Helix, and the Series D was arguably a “downside protection” round (i.e. liquidation preference, priority, etc.) for these holders before Illumina approached Grail regarding an acquisition and/or an IPO.

If true, it raises real questions regarding how arm’s length the Series D process was given the price was being set/influenced by those who would arguably be the biggest beneficiaries of the round, and it also raises concerns regarding the “awareness” of Illumina’s intent to acquire the company after the round.

In particular, the Series D round was bookend by Illumina deconsolidating Helix in April 2019 which potentially removed insider transactions between Helix and Grail being disclosed, and Illumina’s Mostafa Ronaghi was appointed to Grail’s Board shortly after the Series D round was complete and ahead of Illumina CEO Francis deSouza approaching Grail regarding an acquisition.

Illumina deal aside, there’s a case to be made that the exodus of Illumina executive talent around May 2021 may be attributed to realizing an undisclosed financial windfall in Grail through the exercise of a “fair market value” redemption put on February 28, 2021 for Grail equity awards acquired through Helix.

I believe Illumina’s Board has a fiduciary duty to look into this matter, because, if it’s determined this Series D round benefitted Illumina insiders who accumulated their stake via fraud and insider trading through Helix, the offending parties need to be held accountable (i.e. disgorgement of ill-gotten gains) for the legal and regulatory liabilities these alleged violations may have created.

Note: I’m going to using “Helix” and “Helix Holdings I, LLC” interchangeably

Disclaimer: This newsletter is not investment advice. Views or opinions represented in this newsletter are personal and belong solely to the owner and do not represent those of companies that the owner may or may not be associated with in a professional capacity, unless explicitly stated. As previously disclosed, I submitted an SEC whistleblower tip regarding the Illumina situation.

The Illumina-Grail Series

If you haven’t kept up with the Illumina-Grail series (I don’t blame you), check out the “End Notes” in Illumina Discloses SEC Investigation which includes a summary of all the topics I’ve covered to-date that you can explore at your own pace.

Premium Newsletter Plug

If you enjoy this write-up, I hope you consider the Premium Newsletter.

Premium explores “real time” situations and explores interesting governance signals - such as indicators of strategic alteration and other inflective changes - before they potentially happen and/or get priced in.

Professionals: A sensitive subject for many independent newsletter writers is institutions subbing as an “individual” and liberally distributing content internally. Please be reasonable.

UFO Sighting: Dr. Klausner’s Milky Way Investments

The inspiration of the write-up was a simple change in an amended filing.

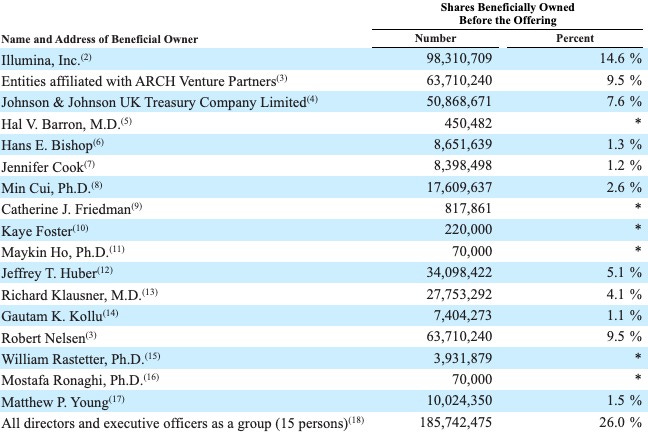

On September 9, 2020, Grail filed their S-1 with the following ownership disclosure:

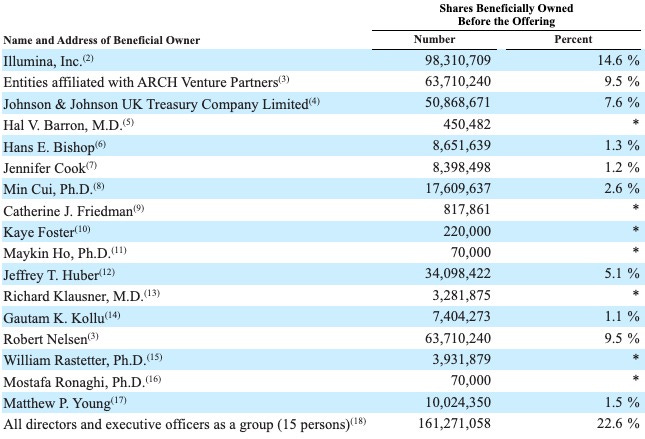

On September 17, 2020, Grail filed an amended S-1/A with an updated table:

Somehow, Dr. Richard Klausner’s beneficial ownership goes from 27,753,292 shares to 3,281,875 shares in a span of ~1 week.

This difference can be explained by the absence of 24,471,417 shares of Series D redeemable convertible preferred stock held by Milky Way Investments Group Limited that was previously included in Dr. Klausner’s beneficial ownership count.

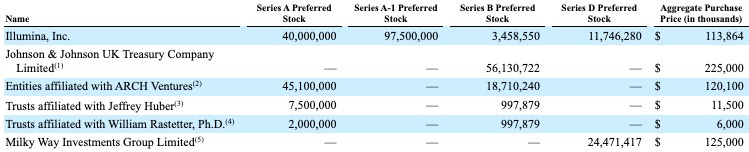

For background, in addition to being a founder and Director of Grail - as well as Illumina’s former Chief Medical Officer - Dr. Klausner is Milky Way’s founder and Managing Partner which invested $125 million in Grail’s $390 million Series D round.

The disappearance of Milky Way’s 24,471,417 shares from Dr. Klausner’s beneficial ownership count has been a massive flag for me, but I couldn’t connect-the-dots to explain “why” it happened until recently and after realizing Helix Holdings I, LLC potentially played a role in Grail’s early financing and insider transactions.

The reason the shares were removed from Dr. Klausner’s beneficial ownership is simple and stated at the top of the ownership table:

To our knowledge, except as indicated in the footnotes to this table and pursuant to applicable community property laws, the persons named in the table have sole voting and investment power with respect to all shares of common stock.

The reason is straight-forward, but tricky part is figuring out why Dr. Klausner would no longer have “sole voting and investment power” of Milky Way’s shares over a ~1-week span, and I think the answer can be found in Grail’s acquisition filing.

The GRAIL Board continued to hold meetings, with members of GRAIL senior management and representatives of Latham and Morgan Stanley also in attendance, on each of September 15, September 16, September 17 and September 18, 2020 to discuss the drafts of the Merger Agreement and other transaction documents exchanged between Latham and Cravath and the relevant open business points, including the collar structure, consideration payable with respect to GRAIL Equity Awards, post-closing bonus payments to GRAIL employees and certain material terms of the CVR Agreement. On September 18, 2020, the GRAIL Board instructed GRAIL management to contact certain GRAIL stockholders who would be requested to deliver support agreements with respect to the transaction with Illumina.

It appears the “sole voting and investment power” of Milky Way’s shares went back to unidentified Grail stockholders during M&A discussions, implying Milk Way was being used by these stockholders to invest in Grail’s Series D round on their behalf.

Milky Way was essentially an “Unidentified Financing Operation” and was arguably not making a bona fide arm’s length investment on behalf of LPs.

Reconciling why existing Grail stockholders would want to collective invest in ~24.5 million Series D shares via Milky Way is where things get interesting - daresay conspiratorial - but I think it makes sense to revisit Helix and build towards why I think Milky Way is a UFO.

The punchline is I believe Milky Way was used by holders of Grail equity awards “transacted” through Helix when formed in 2015 to “lock in” gains and provide “downside protection” via liquidity preference, priority, etc. without disclosing their identity. I believe they don’t want to disclose their identities for the same reasons Illumina didn’t disclose Helix Holdings I, LLC was used to initially fund Grail and distribute equity awards. Illumina insiders (past and present) didn’t want shareholders know the extent of their transactions and involvement at Grail.

Further reinforcing the notion that shares purchased via Milky Way was on behalf of Illumina insiders is the the speed beneficial ownership changed. It demonstrates the funders behind Milky Way’s Series D investment have negotiating leverage to include “sole voting and investment power” terms in the governance documents that quickly revert their rights back to them.

The universe of insiders who would have access to these “Helix” equity awards in the early days, be privy to an acquisition approach, and the rights to ensure beneficial ownership changes so they can vote their interests is a very small group.

Material Grail “Signals” in Helix Disclosures

Realizing that Helix is arguably the “missing link” to help explain how Illumina insiders were able to accumulate a sizable undisclosed equity/economic stake in Grail has really leveled-up my thinking on Grail.

Disclosures I had previously tried to reconcile suddenly made more sense and offered interesting insights when Helix disclosures were viewed through the lens of Grail.

For instance, assuming that the Helix attributed disclosures I’m relying on are indeed Grail-related, you can reconcile how Grail calculated the 112.5 million Class B shares they gave to Illumina when executing a long-term supply agreement:

In January 2016, GRAIL completed its Series A convertible preferred stock financing, raising $120.0 million, of which the Company invested $40.0 million. Additionally, the Company and GRAIL executed a long-term supply agreement in which the Company contributed certain perpetual licenses, employees, and discounted supply terms in exchange for 112.5 million shares of GRAIL’s Class B Common Stock.

Source: Illumina 2016 10-K

Despite the materiality of 112.5 million Class B shares, there isn’t an explanation nor any disclosure to reconcile this transaction in Grail’s S-1 filing. It’s as if the transaction never happened at Grail…

But when you look at Helix disclosures through the lens of Grail, it’s (in my opinion) quite apparent the disclosures are referring to Grail when the entity was formed in 2015:

As contractually committed, the Company contributed certain perpetual licenses, instruments, intangibles, initial laboratory setup, and discounted supply terms in exchange for voting equity interests in Helix. Such contributions are recorded at their historical basis as they remain within the control of the Company. Helix is financed through cash contributions made by the third party investors in exchange for voting equity interests in Helix.

Source: Illumina 2016 10-K

Knowing that Helix was 1) structured as a 50-50 venture, 2) received an equal amount of shares as third party investors, and 3) Grail’s Series A issued 1 share for every $1 invested, we can reconcile the 112.5 million Class B transaction:

Add: $80 million invested by minority investors

Add: $54.167 million cash contribution by redeemable minority investors

Subtract: $21.667 million cash contribution set aside for presumably future options exercise

Total: $80 + $32.5 = $112.5 million invested

We now understand why 112.5 million Class B shares were given to “Illumina”

The point of this tedious example is to show there’s materiality in the tedium of these Helix disclosures they’re treated as a proxy for Grail:

Equity transactions and financings were occurring in Q3 2015 at Helix before Grail was formed and while insiders were still at Illumina. These awards appear to be granted later in 2016 and 2017, etc.

This potentially signals there was a path for Illumina insiders to gain economic/equity exposure in Grail via Helix without disclosure and potentially have those shares delivered at a future date. This could help explain the exodus of talent around noteworthy “Grail centric” dates.

These transactions were treated as redeemable noncontrollable investments from (presumably) “third parties” despite seemingly going to Illumina executives later-on. I don’t know how this was allowed or structured.

Jay Flatley remained an active presence on Helix’ Board until 2019 after stepping down from Grail’s Board in 2017, implying he still had significant influence at Grail despite the disclosures saying otherwise. It may also explain how he had Board Observer rights in a “personal capacity” via Helix.

$10 million dollars worth of redeemable equity awards appear to accelerate vest when Grail does their Series B round and after Grail is deconsolidated from Illumina’s financials. $10 million is potentially 50 million Grail shares getting vested after a year, and a case could be made that this accelerated vesting was intentionally “engineered” with the way the deal was structured through Helix.

This raises serious questions regarding the undisclosed conflicts of interest when Illumina chose to deconsolidate Grail.

Depending on how Grail’s economic/equity interests were structured at Helix, Illumina insiders could conceivably gained Grail exposure via Helix while it was an Illumina consolidated VIE (until Q1 2019).

One thing to keep in mind when thinking about Helix and how it may pertains to Grail’s Series D round is by my guesstimate ~63 million Grail equity awards were “transacted” (i.e. they could have been granted at a future date, but the transaction was executed beforehand) via Helix Holdings I, LLC during the early days:

It’s a large number and I can (generally) only account for ~25 million shares (Jeffrey Huber), meaning ~38 million shares are “out there” somewhere. This is why Milky Way (~24.5 million shares) and Illumina (~11.7 million shares) collectively buying ~36.2 million shares caught my attention.

I can (obviously) keep going with the “Grail” things I’m seeing at Helix so I’ll end this section by saying I didn’t need internal documents or subpoenas to figure out there’s legitimate standing to the idea Helix and Grail are intertwined. I suspect the SEC will probably drill down hard here to understand why Grail’s formation was structured this way, what was hidden from disclosure, and how that impacted the Grail acquisition.

Grail’s 2021 Equity Award Redemption Clock

I believe an extremely under looked issue with Illumina likely using Helix for Grail’s initial funding and to facilitate undisclosed insider transactions is the holders of these “redeemable noncontrolling interest” can compel Illumina to buy their shares at “fair market value” in 2021.

Certain noncontrolling Helix investors may require the Company to redeem all noncontrolling interests in cash at the then approximate fair market value. The fair value of the redeemable noncontrolling interests is considered a Level 3 instrument. Such redemption right is exercisable at the option of certain noncontrolling interest holders after January 1, 2021, provided that a bona fide pursuit of the sale of Helix has occurred and an initial public offering of Helix has not been completed.

In accordance with GRAIL’s Equity Incentive Plan, the Company may be required to redeem certain vested stock awards in cash at the then approximate fair market value. The fair value of the redeemable noncontrolling interests is considered a Level 3 instrument. Such redemption right is exercisable at the option of the holder of the awards after February 28, 2021, provided that an initial public offering of GRAIL has not been completed.

An issue with “fair market value” is Grail’s value is set by Grail’s Board who appear to be controlled by the “redeemable noncontrolling interest” holders. We don’t know the extent of their influence since key governance documents aren’t disclosed, but it seems Illumina’s management could have had meaningful undisclosed econocmic exposure and influence on Grail/Helix - beyond the rights granted to Illumina - through their ownership of redeemable noncontrolling interest.

This means Grail-related decisions done on behalf of Illumina could have very well been led by an executive that held redeemable noncontrolling interest with conflicting interests.

Given that we’re talking about ~63 million Grail shares as well as Helix shares that proxy for Grail shares, this redeemable “put” is a huge liability for Illumina shareholders and they didn’t even know who was potentially conflicted.

It’s not clear to me how these redemption rights “work” following the deconsolidation of Grail in 2017 and the deconsolidation of Helix in 2019. Illumina disclosed they were relieved of any potential redemption obligation for Helix following its deconsolidation, but my immediate thought was, “What’s the catch?” and I’m wondering if those obligations were transferred or negotiated in a way that benefitted holders of Helix noncontrolling interests that were supposed to act on behalf of Illumina’s interests. Nothing (unless I missed it) is mentioned in Illumina’s disclosures regarding Grail’s redemption following their deconsolidation in 2017 which feels like an intentional choice and it seems those rights remained active when you chart the gain in value of Helix value contingent rights in Q1 2021 with the awareness of Grail’s February 28, 2021 redemption put date.

Keep this 2021 “redemption clock” in mind when examining the various decisions surrounding the Grail deal, because I believe these dates influence decision-making at Helix, Grail, and Illumina from 2019 to 2021.

Illumina Deconsolidates Helix in April 2019

When I explored Illumina’s decision to deconsolidate Grail in 2017, I believed they were committing “fraud by omission” to potentially facilitate undisclosed insider transactions of Grail equity/economic interest.

Given my belief that Helix and Grail interests are intertwined, Illumina’s decision to deconsolidate Helix in 2019 is potentially another case of Illumina insiders committing “fraud by omission” to facilitate undisclosed insider transactions:

On April 25, 2019, we entered into an agreement to sell our interest in, and relinquish control over, Helix. As part of the agreement, (i) Helix repurchased all of our outstanding equity interests in exchange for a contingent value right with a 7-year term that entitles us to consideration dependent upon the outcome of Helix’s future financing and/or liquidity events, (ii) we ceased having a controlling financial interest in Helix, including unilateral power over one of the activities that most significantly impacts the economic performance of Helix, (iii) we were relieved of any potential obligation to redeem certain noncontrolling interests, and (iv) we no longer have representation on Helix’s board of directors.

If they felt they “got away with it” in 2017 with Grail, you shouldn’t be surprised if they felt they could do it again with Helix in 2019.

Regardless of the Helix deconsolidation, if you believe Helix and Grail are truly intertwined, there are material omissions in the existing disclosures that make Helix very misleading to shareholders since they don’t address their involvement with Grail in the early days and the obligations between the two entities. An argument could even be made that the creation of Helix and its messaging to shareholders was intentionally deceptive for insiders to accumulate undisclosed shares in Grail.

Further reinforcing the “intertwined” dynamic between Illumina, Grail, and Helix, I don’t think it’s happenstance that Illumina suddenly starts disclosing Grail as a VIE (again), without mentioning them by name (of course), after Helix is deconsolidated:

One of our non-marketable equity investments is a VIE for which we have concluded that we are not the primary beneficiary, and therefore, we do not consolidate this VIE in our consolidated financial statements. We have determined our maximum exposure to loss, as a result of our involvement with the VIE, to be the carrying value of our investment, which was $190 million and $189 million as of December 29, 2019 and December 30, 2018, respectively, recorded in other assets.

This potentially implies Grail’s undisclosed governance documents includes Helix - or Helix affiliated entites - as a party to the agreement in some form and the Helix deconsolidation changed Illumina’s accounting treatment of Grail.

A key concern I have with Illumina’s April 2019 deconsolidation of Helix is Grail would subsequently raise their Series D round in November 2019, and the number of shares purchased by Milky Way and Illumina seem to align with the number of “unaccounted” equity awards “transacted” through Helix in 2015. If there were any “related party” transactions involved as part of the Series D (i.e. pledging shares to purchase Series D stock via Milky Way) to fund the round, they won’t be disclosed following the Helix deconoslidation. This raises a serious red flag regarding the motives of Illumina’s Board and executive team to deconsolidate Helix and whether or not they’re serving the interest of shareholders.

Disclosure-Based Conspiracy: Grail’s Series D Round

With the aforementioned in mind, when reviewing the mosaic of disclosures and behavior of insiders, the notion that Grail’s Series D round was used used to “lock in” gains and provide “downside protection” on deep in-the-money equity awards (via Helix) during Grail’s early days doesn’t seem conspiratorial to me. Things seem to happen in plain sight since there’s (in my opinion) a perception by Illumina insiders that no one realizes Helix is involved with Grail.

For starters, Dr. Rick Klausner’s $125 million Series D investment felt so “out of the blue” it didn’t feel right.

He’s a central figure in Grail’s formation and was involved from the beginning, and you’re telling me that he “only” received ~3.8 million shares per the S-1/A disclosure?!

The only thing more incredulous to me is Illumina trying to say Jay Flatley didn’t have any financial exposure to Grail. Consequently, I’m operating under the belief there are additional shares that benefit Dr. Klausner and Mr. Flatley elsewhere.

Often times, “world class” governance and investment analysi is keeping things simple, noticing there’s an elephant in the room, and just keep “throwing peanuts” at the elephant until everyone else notices.

Rant aside, the actual “problem” with Milky Way’s $125 million investment is it appears to be the “first money” in the Series D round, and Grail intentionally doesn’t mention them despite taking down 1/3 of the round:

New investors including Public Sector Pension Investment Board (PSP Investments) and Canada Pension Plan Investment Board (CPP Investments), as well as two undisclosed investors, joined existing backers including Illumina, Inc. in this round of funding.

Given my belief Milky Way was used as a vehicle to purchase shares by other insiders to remain undisclosed and retained the option to reclaim “sole voting and investment power”, the optics of self-dealing potentially occurring among insiders with this transaction is glaring.

What’s also interesting about the timing of the Series D round is throughout 2019 leading up to the initial Series D funding, Grail was modifying options (i.e. accelerated vesting, extending term, changing performance conditions, etc.). This is important for a few reasons:

Holders may not grant a lien or security interest in, or pledge, hypothecate or encumber UNVESTED options. Options need to be vested for pledging purposes.

If an Employee owns or is deemed to own more than 10% of the combined voting power of all classes of stock of the Company or any Subsidiary or Parent of the Company, and an Incentive Stock Option is granted to such Employee, the term of such Option shall be no more than five (5) years from the date of grant. The folks getting extended are likely large holders and/or part of a group with a large holding (i.e. options granted in 2016 via Helix).

It signals the Board is coordinating with key holders in anticipation of them using pledged options to finance their Series D investment. Keep in mind pledging shares still requires Board approval and must meet certain requirement.

The level of planning and coordination among Grail insiders raises serious questions regarding the potential intent and/or conflicts of various decisions/disclosures at Illumina and by Illumina insiders leading up to the Series D round, and Illumina’s subsequent approach to acquire the company:

Helix is deconsolidated in April 2019 just ahead of Grail modifying options and raising a Series D round. Illumina is arguably negotiating with Illumina insiders who hold redeemable noncontrolling interest in Helix, and raises questions on how arm’s length the terms of the deconsolidation are.

Illumina’s Marc Stapley leaves to serve as CEO of Helix in April 2019 (where he was already serving as Director since 2015) after Jay Flatley steps down Helix’ Board and Helix is deconsolidated.

Mr. Stapley’s CEO tenure at Helix is from April 2019 to May 2021 which aligns with Grail’s Series D, Illumina’s acquisition announcement, and the February 28, 2021 redemption date to sell equity awards back to Illumina at “fair market value”. I believe he was serving as CEO of Helix Opco, but I suspect his primary objective and incentives at Helix were tied to Grail.

Following Grail’s Series D round, Illumina’s Mostafa Ronaghi joins Grail’s Board on May 4, 2020 and would leave Illumina in January 2021 around the same time Helix’ January 1, 2021 redemption rights would have been available prior to Illumina’s deconsolidation and before the February 28, 2021 redemption period for Grail equity award holders.

Chief Accounting Officer Karen McGinnis announces her plans to retire on August 19, 2020 while Illumina is in the middle of deal discussion with Grail with an effective date of April 1, 2021, after the February 28, 2021 redemption date.

Jay Flatley changes his role from Executive Chairman to Chairman (non-employee status) effective January 1, 2020 right when Grail is in the middle of raising their Series D round, and announces on March 18, 2021 his intent to leave Illumina’s Board effective May 26, 2021.

Director Robert Epstein’s reported ownership of Illumina stock magically increases by 1,000 shares without explanation on May 27, 2021 which approximates to the number of shares a Grail Director would receive in exchange for 70,000 Grail (he served as a Board observer at Grail in 2017). He also serves on the Board of Veracyte (Chairman) where Marc Stapley is appointed as CEO on June 1, 2021. Former Illumina Director Karin Eastham also serves on Veracyte’s Board and departed Illumina’s Board in May 2019.

Maybe this is just conjecture, but the disclosures indicate to me Helix Holdings I, LLC was involved with Grail leading up to the Series A round and there are Helix disclosures that reconcile with Grail disclosures extremely well (if not perfectly). This raises serious questions regarding how Illumina disclosed their Helix VIE to shareholders and why Illumina deconsolidated Helix ahead of Grail’s Series D round. Both Illumina’s new Directors and the SEC should investigate this. This is a legitimate liability for Illumina shareholders.