SPACémon: Gotta List 'Em All!

On "Pokémon" Governance, SPACs, and The "Go Public" Process

Welcome to the Nongaap Newsletter! I’m Mike, an ex-activist investor, who writes about tech, corporate governance, the power & friction of incentives, strategy, board dynamics, and the occasional activist fight.

If you’re reading this but haven’t subscribed, I hope you consider joining me on this journey.

For this write-up, I’m discussing 3 topics:

“Pokémon” Governance: Inspired by Stripe co-founder John Collison and his “board members are Pokémon” analogy, I discuss the importance of complementary skillsets at the Board level.

SPACs: I share some governance thoughts on SPACs (spoiler: expect more Pokémon references), and why companies shouldn’t settle for average.

The “Go Public” Process: Inspired by a tweet from Shopify CEO Tobi Lütke, I discuss how a company earns “long term” trust in public markets. I’ve noticed the first 2 to 5+ years of public company life often mirrors Paul Graham’s The Process curve, and share my “go public” version of this journey.

This was a fun one to write!

Note: Like Pokémon, each SPAC sponsor has unique strengths and weakness to offer a company. Pictured (for fun, not hating): PikAckchu, MasaSquirtle, BillFoleysaur, Chamathmander

“Pokémon” Governance

Stripe co-founder John Collison was recently a guest on the terrific Invest Like the Best podcast and was asked about his views on Board members and governance:

Question: I’m curious what you think Board members should do, and in your experience, if you’ve had a great one or two, what they’ve done for Stripe.

John Collison: I mean, we’ve been lucky to have incredible Board members. And I think part of…They’re all different Pokémon, with different strengths and weaknesses and attacks and such like that. And so I think it’s important for the Board member to know what they are providing, and for the companies know what they should be getting from the Board member.

I love this answer and wish I came up with this Pokémon analogy. No really…

Whether you’re an investor or executive, it’s critical to assess the strengths and weaknesses of each Board member and how they complement the rest of the Board, the company, and long-term priorities.

Over the course of a company’s life, these directors will be called upon (like Pokémon!) to use their unique skills and experiences to navigate difficult situations and/or elevate the company. If certain skills are lacking, or certain perspectives are overrepresented, the company risks long-term value destruction.

Most understand the importance of diverse skillsets and perspectives, but I can’t emphasize enough how destructive “overrepresented perspectives” can be. You get a couple individuals dominating the Board’s agenda and it doesn’t matter how differentiated and complementary the rest of the Board is. Those other members never get an opportunity to fully contribute.

It’s like having Team Rocket in the Board room disrupting things. It’s also the source of a lot of corporate governance “dark arts” shenanigans.

That said, other directors typically don’t raise a fuss about this dynamic due to collegial culture and not wanting to rock the boat, but the sentiment is there (in my opinion). You tend to see frustration expressed year-after-year in PwC’s Annual Corporate Directors survey as many secretly want fellow directors replaced:

Directors want refreshment, but boards fail to plan for the next chapter.

Boards are making strides in many areas, yet their own composition remains one of the toughest challenges for boards to confront. For the second year in a row, about half (49%) of directors say that at least one fellow director on their board should be replaced. Twenty-one percent (21%) say that two or more directors should go. These numbers remain high, despite intense shareholder focus on board refreshment.

What stands in the way of board refreshment? Many directors point to board leadership’s unwillingness to have difficult conversations with underperforming directors (20%) or to an ineffective assessment process (19%).

In order to build a Board with complementary skillsets and perspectives, activist investor and corporate governance pioneer Ralph Whitworth advocated looking at Board vacancies in a “dynamic way” and on a multi-year time horizon:

Look at the Board composition in a dynamic way. Committees are taking a narrow view on addressing vacancies on a year-to-year basis instead of taking a 5-year outlook and setting criteria and objectives on that basis. You begin to realize there are actually 4-5 “vacancies” on any Board.

Even if directors aren’t replaced, this approach is an opportunity to highlight areas of need and give members a chance to evolve and work on their skillsets to better address those deficiencies.

Overall, the entire John Collison episode is worth listening to, but this was my other favorite (governance) highlight from the podcast:

John Collison: First and foremost, obviously [board member] is a governance role. You are managing the management team.

And I think there’s a… Buffett called this out in his, I think it was his letter this year, complaining about the cozy relationship between board members and management at company.

But I think that is an important aspect of it, which is, board members need to realize that they work for the shareholders, and they are the boss of the management and not the other way around. And I think ones that internalized that relationship, tend to be the most effective.

And look, that’s generally pretty friendly because oftentimes the best way to help the shareholders is to help the management, but there can be no confusion about that.

Stripe still has to “walk the walk”, but this shareholder friendly tone to governance will go a long way in building a long-term support base when the company goes public.

SPACs

Regardless of your views on SPACs, I think we can all agree it’s important to acknowledge the potential distorting effects of this SPAC boom on private markets and the accompanying conflicts of interest that may arise at the governance level.

After all, if board members are like Pokémon with strength and weaknesses, then misaligned incentives is a major weakness.

These misaligned incentives can nudge Boards members and executives towards short-term personal/professional considerations over long-term company considerations.

It’s helpful to acknowledge the temptation of accepting a generous SPAC offer from a sponsor that is an average-to-bad fit for the company long-term.

If companies and founders are considering a SPAC, I believe they should not be settling for average fit (let alone bad).

From a governance perspective, SPACs can and should be a way to source a superstar director (call them a Legendary Pokémon if you will) to help the company. That should be the bar, especially when the accompanying promote fee is compensating them like a superstar. Of course, the question is what’s considered “superstar”? That’s entirely dependent on the company, its needs, and long-term priorities.

Generally speaking, when a company goes public via SPAC, a new (and powerful) director is added to the Board by the SPAC. This new director typically takes on a lead director type role (Chairman, Vice Chairman, etc.) and serves as a driving force at the Board and company. If there’s any uncertainty about the SPAC director’s ability to play this role, keep looking.

Again, this is a chance to really kickstart the company’s public journey and have someone in place to be a steward and help the founder/CEO drive the vision forward. If a company is about to take on that governance burden, the bar should be high.

The “Go Public” Process

Shopify CEO Tobi Lütke recently tweeted that “being public and trusted is the best possible state for a company”.

I wholeheartedly agree with this sentiment, but easier said than done. It has to be earned through steady execution over years and there aren’t short-cuts.

So what does earning “long term” trust in public markets look like?

I’ve thought a lot about this over the years and (in my opinion/experience) the journey to building “long term” trust can often look like Paul Graham’s startup curve (aka “The Process):

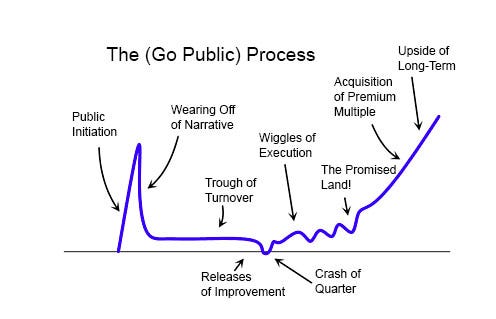

I present to you The “Go Public” Process:

Note: This is personal opinion based on my experiences researching and investing in public software/technology companies.

Each public company has their own timeline, but I generally believe a public company’s valuation isn’t “real” until 18-24 months after going public, and it can take another 18-24 months to truly prove out the operating model and earn “long term” trust.

I don’t care how long a company has operated as a private company. There are certain “public company” muscles that are never properly exercised as a private company and must be developed while public.

Over the initial 2 to 5+ years, there are some notable milestones/checkpoints I’ve noticed many companies experience before achieving “long term” trust. Let’s walk through them.

The “Go Public” Process:

Public Initiation: The first day “IPO Pop”. This is peak enthusiasm for the company and its potential. This is the most “manufactured” stage of a company’s public life. From the cookie cutter metrics to the cookie cutter messaging, everything is a beauty contest meant to appeal to rule-of-thumb checklists, heuristics, rule-of-40, and everything else featured in an S-1 teardown.

Wearing Off of Narrative: Eventually reality set sin. Company continues to grow and execute, but any-and-all pessimism will wear on the stock. They might miss on cookie-cutter expectations and vanity metrics, but they weren’t really operating the company on those metrics anyway. Concerns over TAM and big tech competition wears on the stock as well.

Trough of Turnover: Going public is a low key restructuring. Some lucky companies don’t see excessive turnover, but when the lock-up expires investors and employees are leaving. CEO/founder is rebuilding leadership team and Board. A lot of the cookie-cutter advice and suggestions tends to walk out the door during this period.

Releases of Improvement: Pretty much the same as before. Company is still releasing improvements and executing.

Crash of Quarter: At some point there’s a crash. It’s usually a missed quarter. The business is still improving and growing, but it’s all about expectations. This is where there’s capitulation and possible talk of “busted IPO”. At this point, companies refocus on first principles and nailing down the metrics that actually matter. Toss out the cookie cutter metrics and guidance. This is where the true “North Star” is identified and new priorities are set. Sell-offs create focus.

Wiggles of Execution: Company implements, communicates, and executes the new “North Star” plan. Things are beginning to improve internally (often at an accelerating rate) and the business is making big strides. That internal momentum is not getting properly reflected in the financials and/or metrics. Stock remains lumpy since execution is lumpy. There’s a lot of de-risking that occurs during this period. New investors begin rolling in who will represent the foundation of your “long term” base.

The Promised Land!: Your “North Star” plan finally starts producing meaningful financial results. The stock pops. If they don’t make it to the “promised land”, the company might fork over to strategic alternatives land (the strategic and financial buyers were chatting up the company this whole time).

Acquisition of Premium Multiple: The financials and key metrics continues its upward momentum and the valuation experiences premium multiple expansion as the business compounds. At this point, the CEO begins to shift focus to longer-term projects. This may include raising capital to help accelerate timelines.

Upside of Long-Term: Welcome to Day 1 of escape velocity. Company has earned “long term” trust in public markets to pursue long-term goals.

Obviously this is generalized and each company’s journey is different, but I live for investing in the “wiggles of execution” stage. It’s the point where CEOs/founders find their voice in public markets and shine.

SNAP exemplifies your diagram well

Starcraft and Pokemon. Can we expect an MTG take soon?