In our last episode of Silicon Valley B., I flagged and explored 2 common knowledge* issues:

SVB didn’t have a Chief Risk Officer (CRO) for much of 2022.

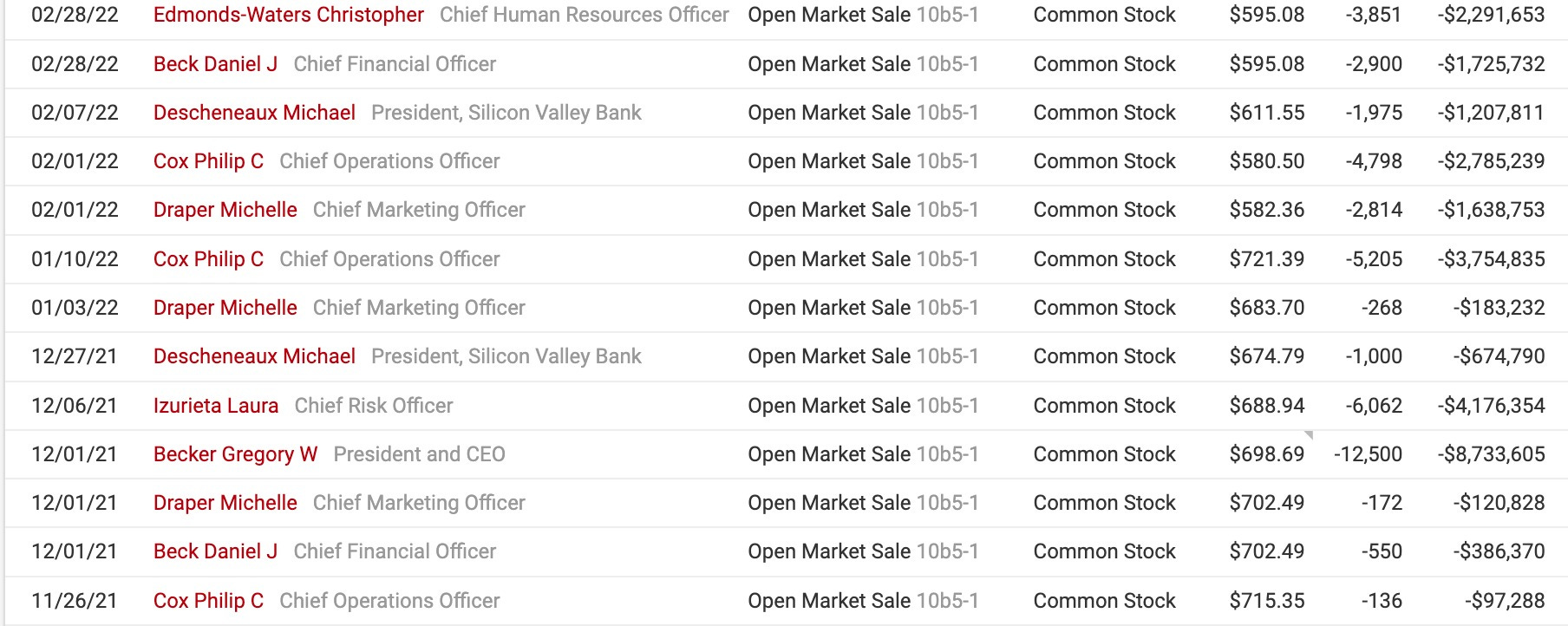

CEO Greg Becker sold shares in February 27, 2023 under a 10B5-1 Plan that had a 30-day “cooling off” period (i.e. the plan was implemented on January 26, 2023).

Both the missing CRO and executive trades are major talking points in the SVB saga and being probed by regulators.

For this episode, I explore:

Seemingly incorrect/missing company disclosures.

The Risk committee arguably making “CYA” amendments to their charter.

The puts-and-takes of tying executive compensation to ROE.

SVB signaling risk management issues in 2022 via company disclosures.

Simply put, a case can be made SVB’s management and Board parlayed incompetence into an alleged cover-up with prosecutorial consequences.

* As Rodney Dangerfield would say, “That’s the story of my life. No respect!” In the dog-eat-dog world of journalism, using “common knowledge” facts isn’t considered plagiarism nor requires attribution. Never mind no one noticed these facts until I brought them up and I have a premium newsletter literally built on the market not properly pricing in “common knowledge” governance disclosures. Anyway, I look forward to mass media outlets independently “discovering” the findings in this write-up without attribution.

Disclaimer: This newsletter is not investment advice. Views or opinions represented in this newsletter are personal and belong solely to the owner and do not represent those of companies that the owner may or may not be associated with in a professional capacity, unless explicitly stated.

Support My Solvency: Join Premium

If you enjoy this write-up, consider subscribing to the Premium Newsletter.

Premium explores “real time” situations and looks for interesting governance signals, like indicators of strategic options and other noteworthy inflections, before they potentially happen and/or gets priced in.

Note:If you previously subscribed to premium, a friendly reminder you were issued a pro-rated refund in February 2022 and will need to re-subscribe to receive premium emails again.

SVB: Available-FUD-Sale

With regulators now in charge of Silicon Valley Bank (SVB) following its historic failure, everyone is trying to unpack what exactly happened, how did things fall apart so quickly, and who’s to blame.

There are many ways to tranche (pun intended) what happened, but it appears an accumulation of seemingly minor transgressions and bad decisions compounded into the failed outcome we see today.

Individually, these transgressions and decisions might not have killed the company, but a “perfect storm” formed and ultimately sunk the entire ship.

Interestingly, had management and the Board done the “right thing” early on, an argument could be made the company would have survived.

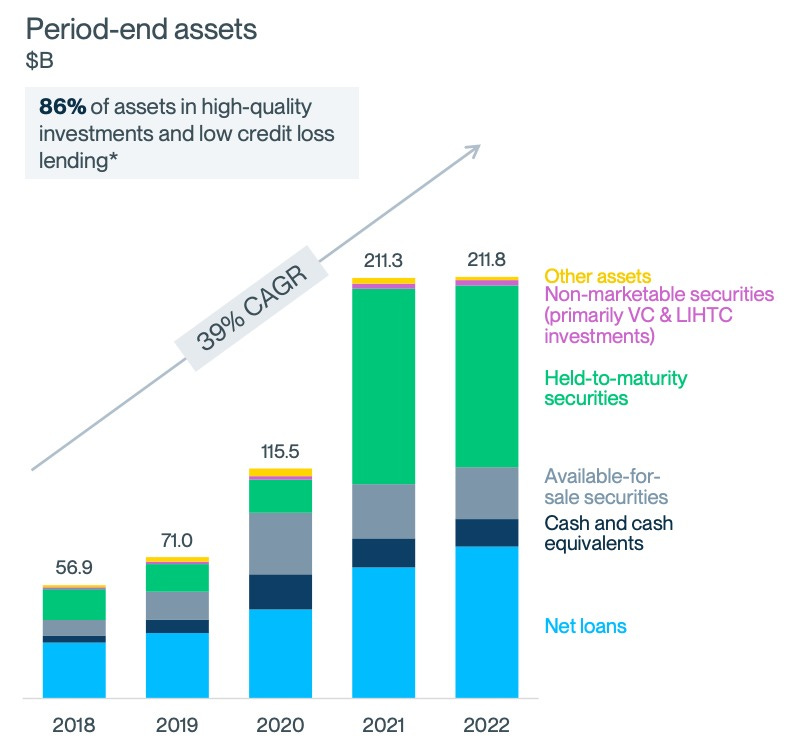

Category IV (Balance Sheet) Hurricane

There’s plenty of coverage and debate regarding the regulatory requirements (or lack thereof) that caused SVB to fail, but there doesn’t seem to be much attention nor discussion on the impact of SVB becoming a “Category IV” bank (with more stringent and specific regulatory oversight mandated on the Risk Committee) in 2022:

Under the Tailoring Rules, banking organizations are grouped into four categories based on their U.S. G-SIB status, size and four other risk-based indicators. The most stringent standards apply to U.S. G-SIBs, which represent Category I, and the least stringent standards apply to Category IV organizations, which have between $100 billion and $250 billion in average total consolidated assets and less than $75 billion in certain other risk-based indicators. Category IV organizations are, among other things, subject to: (i) certain liquidity risk management and risk committee requirements, including liquidity buffer and liquidity stress testing requirements, (ii) requirements to develop and maintain a capital plan on an annual basis and (iii) supervisory capital stress testing on a biennial basis. SVB Financial is considered a Category IV organization, and accordingly, is subject to requirements applicable to Category IV organizations.

Source: SVB 2022 10-K

As of June 30, 2021, SVB passed the $100 billion Category IV threshold as of June 30, 2021 meaning they’d be subject to “more stringent” requirements applicable to Category IV institutions in 2022 (i.e. fifth quarter after passing $100 billion threshold):

Initial applicability. Subject to paragraph (c) of this section, a bank holding company must comply with the risk-management and risk-committee requirements set forth in § 252.33 and the liquidity risk-management and liquidity stress test requirements set forth in §§ 252.34 and 252.35 no later than the first day of the fifth quarter following the date on which its average total consolidated assets equal or exceed $100 billion. (Federal Regulations)

For SVB, the most consequential change of being a Category IV organization was making the Board’s Risk Committee responsible for liquidity risk-management oversight:

General. A bank holding company subject to this subpart must maintain a risk committee that approves and periodically reviews the risk-management policies of the bank holding company's global operations and oversees the operation of the bank holding company's global risk-management framework. The risk committee's responsibilities include liquidity risk-management as set forth in § 252.34(b). (Federal Regulations)

The Finance Committee actively oversees our capital and liquidity management and the associated risks (whether as an ongoing matter or as it relates specifically to a transaction, such as an equity or debt securities offering). (2021 SVB Proxy)

Our Asset/Liability Committee (“ALCO”), which is a management committee, provides oversight to the liquidity management process and recommends policy guidelines for the approval of the Finance Committee of our Board of Directors, and courses of action to address our actual and projected liquidity needs. Additionally, we routinely conduct liquidity stress testing as part of our liquidity management practices. (2021 Annual report)

Shifting oversight to the Risk Committee is quite significant given the Chief Risk Officer has much more regulatory power and independence on liquidity risk-management matters.

Also, the Risk Committee consists of Board committee chairs making it harder for directors to completely bury their head in the sand on liquidity risk-management issues, and there’s also more stringent regulatory oversight requirements relative to the Finance Committee:

Our ALCO, which is a management committee, provides oversight to the liquidity management process and recommends policy guidelines for the approval of the Finance Committee andRisk Committee of our Board of Directors, and courses of action to address our actual and projected liquidity needs. Additionally, we routinely conduct liquidity stress testing as part of our liquidity management practices. (Q1 2022 Filing)

This shift in oversight could potentially explain why Laura Izurieta vacated the Chief Risk Officer role in 2022. Either she or the Board or both wanted no part in the oversight responsibilities, especially given the sudden ramp in held-for-maturity securities that occurred on the balance sheet in 2021 that arguably required addressing in the face of rising interest rates:

This, in turn, is going to draw a lot of attention to what insiders knew on this liquidity issue and when given they collectively unloaded millions of dollars in stock from late 2021 to early 2022 (especially CEO Greg Becker and CRO Laura Izurieta):

While the company “routinely conduct[s] liquidity stress testing as part of [their] liquidity management practices”, there’s going to be a lot of scrutiny over how this was handled through the Finance Committee if the Risk Committee and Chief Risk Officer wasn’t actively involved in the oversight process, especially when held-to-maturity securities materially ramped in 2021. It’ll also raise questions on how this issue was handled in 2022 given the absence of an independent Chief Risk Officer.

Navigating Risky Unchartered Waters with “CYA” Changes

Now, SVB’s Board and management team will likely argue liquidity risk-management was appropriately handled despite having no Chief Risk Officer for much of 2022, but amendments to the Risk Committee Charter arguably imply this was a “hot potato” issue and the Board was in CYA mode as a result.

The April 2022 Charter curiously changes the language from “ensuring” to “assessing” the independence of the Company’s risk management function to lighten the Risk Committee’s oversight burden:

Ensuring the independence of the Company’s risk management function

Assessing the independence of the Company’s risk management function

The Risk Committee also amended the Charter so they can effectively rely on information at “face-value”:

Dependence on information: In carrying out its oversight responsibilities, each Committee member shall be entitled to rely on the integrity and expertise of those persons providing information to the Committee and on the accuracy and completeness of such information, absent actual knowledge of inaccuracy.

Basically, the Risk Committee gave management permission to “vouch” for the independence of company’s risk management function and was allowed to take their word at face-value as long as the Committee didn’t know the statements being made were inaccurate! Seriously!

This is the kind of amendment that would allow management to essentially delay addressing their balance sheet in 2022 by simply saying it doesn’t need to be addressed in the absence of an independent Chief Risk Officer who is appointed by the Risk Committee, directly reports to the Risk Committee, and is responsible for reporting risk-management deficiencies.

It’s as if the Risk Committee knew having no Chief Risk Officer was problematic and made “CYA” amendments to the Risk Charter to cover their bases.

It’s Not the Incompetence, It’s the (Alleged) Cover-Up

What makes this “missing Chief Risk Officer” situation go from bad to worse are the incorrect/missing company disclosures of former CRO Laura Izuriet’s departure.

First, keep in mind that Ms. Izurieta ceased serving as Chief Risk Officer as of April 29, 2022:

Ms. Izurieta departed the Company on October 1, 2022. The Company initiated discussions with Ms. Izurieta about a transition from the Chief Risk Officer position in early 2022. Accordingly, the Company and Ms. Izurieta entered into a separation (without cause) agreement pursuant to which she ceased serving in her role as Chief Risk Officer as of April 29, 2022 and moved into a non-executive role focused on certain transition-related duties until October 1, 2022. (2023 Proxy)

So when a Form 4 was filed on May 5, 2022 for Ms. Izurieta, it incorrectly labeled her title as Chief Risk Officer. Maybe it was incompetence on Wei Sun’s part (who signed the transaction as attorney-in-fact) or maybe her employment status was not widely known within the company to cause the error in the filing.

Also, the company disclosed Ms. Izurieta was a Named Executive Officer in 2022:

Named Executive Officers

For 2022, our named executive officers (“NEOs”) are Mr. Greg Becker, President and Chief Executive Officer; Mr. Dan Beck, Chief Financial Officer; Mr. Michael Descheneaux, President, Silicon Valley Bank; Mr. Philip Cox, Chief Operations Officer; and Mr. Michael Zuckert, General Counsel. Our NEOs for 2022 also include Ms. Laura Izurieta, former Chief Risk Officer, who departed the Company in October 2022 and ceased serving in her role as Chief Risk Officer on April 29, 2022. (2023 Proxy)

As pointed out by Michelle Leder of Footnoted, being a Name Executive Officer should have triggered an 8-K filing when Ms. Izurieta departed:

Now here's where it gets pretty interesting: Izurieta was a "named executive officer" of the bank, which means that her departure as Chief Risk Officer should have triggered an 8-K. (Footnoted)

The SEC's rules are pretty clear on this:

So why wasn’t her departure disclosed?

General Counsel Michael Zuckert, who, by the way, received a 90% payout on his 2022 annual bonus (highest payout among Named Executive Officers), has some explaining to do…

As an aside, I also find it interesting that long-time executives, and 2021 Named Executive Officers, John China (President of SVB Capital) and Marc Cadieux (Chief Credit Officer) are noticeably absent from the 2023 Proxy, and don’t have any Form 4 transactions reported since January 2021. If they were Named Executive Officer in 2021, the company should have filed Form 4 transactions throughout calendar 2021, including equity grants that executives annually receive.

Was the company trying to avoid not disclosing something material in the 2023 Proxy by removing Messr. China and Cadieux as Named Executive Officers?

Overall, the optics look awful and gives the impression the company was actively trying to cover-up risk management issues at the company by shuffling Named Executive Officer designations year-to-year.

Ruh-ROE! We Have an Incentives Problem!

Setting aside the aforementioned Chief Risk Officer and disclosure issues, why in the world would management be so reluctant to make much needed changes to their balance sheet and address their held-to-maturity security holdings as rates climbed?

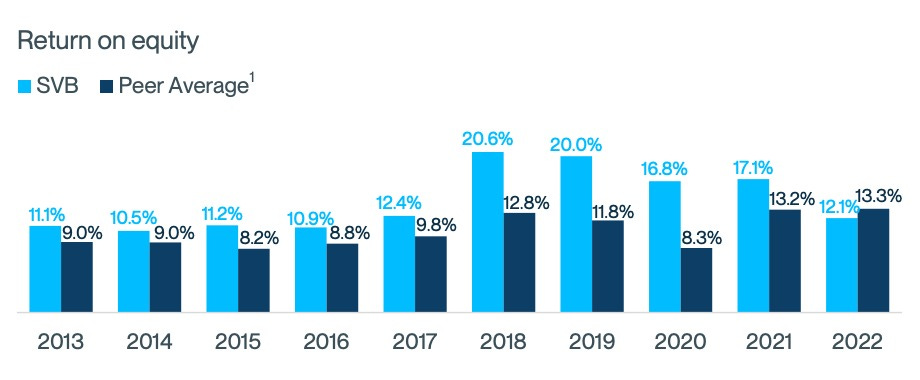

It seems so simple, but I think management had an incentives problem. Specifically, compensation was heavily geared towards ROE which were spectacularly high the past few years due to their capital allocation decisions, and management was getting rewarded handsomely as a result:

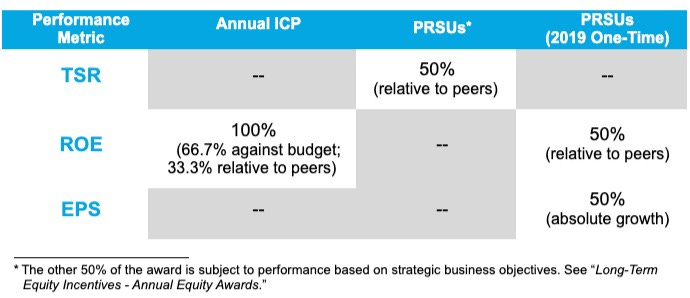

As further discussed in this CD&A, specific performance metrics for recent annual and long-term incentive awards include ROE and TSR, and in certain cases our performance is measured relative to peer performance. More specifically, ROE is a performance metric for both our annual ICP funding and PRSU awards. This is an intentional design by the Comp/HC Committee because it believes that ROE is the most appropriate indicator of our short-term and long-term financial performance as it demonstrates how efficiently the Company is using capital invested by shareholders to generate profit. We use ROE both on an absolute basis and relative to peers. While the Comp/HC Committee has considered other more absolute measures of earnings (e.g., EPS or Net Income) in place of ROE in either the long-term or the short-term plan, the committee believes ROE is a preferred metric to assess profitability and shareholder return. (2023 Preliminary Proxy)

To be fair, ROE is considered a consensus metric in both compensation and evaluating financials so you can’t necessarily knock them for using it.

On the other hand, the focus on 1 to 3 year ROE as a key metric created a dangerous situation for SVB given the rapid growth of non-interest-bearing deposits. In order to achieve desired ROE within this 1 to 3 year timeframe, the company needed to deploy capital into longer duration securities to generate the yield necessary to achieve their desired return.

The trade-off is SVB was essentially generating “risk-unadjusted” ROE which created a riskier and more volatile return profile for the company since it required taking on more risk to generate the desired ROE over 1 to 3 years.

Investors love ROE, but it has to be risk-adjusted ROE and reflect the structural long-term advantages a business has. SVB certainly had an advantage vs. peers with their enviable positioning within the Silicon Valley ecosystem, but it introduced pronounced deposit flow cyclicality that made 1 to 3 year ROE arguably a fragile compensation metric to use. The Compensation Committee probably needed to rethink and evolve how to reward management in the face of this cyclicality, but didn’t.

Consequently, this 1 to 3 year ROE tilt to compensation may have also potentially played a role in management’s reluctance to make changes going as far back as late 2020 before non-interest bearing deposits began to really ramp:

In late 2020, the firm’s asset-liability committee received an internal recommendation to buy shorter-term bonds as more deposits flowed in, according to documents viewed by Bloomberg. That shift would reduce the risk of sizable losses if interest rates quickly rose. But it would have a cost: an estimated $18 million reduction in earnings, with a $36 million hit going forward from there.

Executives balked. Instead, the company continued to plow cash into higher-yielding assets. That helped profit jump 52% to a record in 2021 and helped the firm’s valuation soar past $40 billion. But as rates soared in 2022, the firm racked up more than $16 billion of unrealized losses on its bond holdings. (Bloomberg)

This, in turn, may have contributed to held-to-maturity securities meaningfully ramping beginning in Q1 2021:

As the saying goes, “Show me the incentive and I’ll show you the outcome.” In many ways, SVB became a victim of its own success.

Nothing to SEE Here…

This alleged reluctance to address the balance sheet and its impact on ROE was further exasperated by one-time equity awards granted to management in 2019 that were slated to vest at the end of 2021 (certified in January 2022):

Special One-Time Executive Equity Awards (SEE Awards)

A top priority for the Compensation Committee in 2019 continued to be driving long-term performance over the next several years, and incentivizing and retaining our executive leadership team, who are critical to the Company’s continued growth and success. At the time the SEE awards were considered and approved in 2019, the Board and Compensation Committee took note of the Company’s exceptional performance under the executive team over the past few years, as well as the potential retention risk in the highly-competitive banking industry. The Compensation Committee considered the strong historical performance, particularly between the years 2015 and 2018, during which the Company increased over the multi-year period:

annual net income by 183%;

annual average total assets by 35%;

annual average total loans, net of unearned income, by 74%; and

annual average total client funds by 63%.

Accordingly, the Compensation Committee (and in the case of the CEO’s compensation, the Board) believed it was important to grant our executives, including our NEOs, the SEE awards, which were designed to be primarily performance-based, subject to three-year performance and cliff vesting. These awards add additional incentives for our executives to achieve high performance through the use of PRSUs (50%) and stock options (25%), as well as help to reinforce retention of our executive team through the use of RSUs (25%).

PRSUs under the SEE awards are subject to vesting over a 3-year period (from 2019-2021) based on two performance metrics, different from the annual PRSUs, as further discussed below: (i) EPS growth, and (ii) ROE relative to peers. To the extent earned as determined by the Compensation Committee (or the Board), these awards are subject to additional time-based vesting through January 31, 2022.

With this in mind, a case could be made management was aware of the balance sheet issues in 2021, but hard decisions to address them were held off/delayed to ensure these one-time SEE Awards as well as other awards vested at max payout:

Upon completion of the 3-year performance period, the Comp/HC Committee (and in the case of the CEO, the Board) determined 150% of the target SEE Awards were earned for each of the NEOs, based on (i) the Company’s achievement of an EPS CAGR of 24.7% as determined by the committee and (ii) the Company’s outperformance of ROE relative to its peers (ranking first).

I know it seems like I’m overly focused on the influence of (short-term) ROE in management’s decision-making, but consider the company was making adjustments to ROE (tied to “budgeted ROE” in their annual bonus) that excluded a “budgeted capital raise” in 2022 that was presumably intended to start addressing their balance sheet issues:

Additionally for 2022, the committee approved the exclusion of (i) certain expenses related to the Boston Private merger, including merger related expenses; and (ii) budgeted equity capital raise. (2023 Proxy)

So when the company announced their plans to raise capital in 2023 which would crater 2023 ROE guidance to ~2% (and trigger a run on the bank), it doesn’t go over my head that the announcement was done after 2022 compensation was certified in January 2023 which would have impacted relative TSR calculations (which was the other metric management was compensated against) for performance-based equity payouts:

Again, relative TSR isn’t a “bad” metric, but at a time when the company was facing a “perfect storm” of issues, this metric goes from “generally good” to “existentially bad”.

Board Signaling Risk Management Issues?

Finally, the 2023 Proxy and 2022 governance documents offer a treasure trove of disclosures that seem to signal the Board was well aware there were risk management issues at the company and was quietly trying to address them in 2022.

For instance, the April 2022 Risk Committee noticeably includes specific language on instilling a “risk culture” at the company:

Risk culture: In coordination with the Compensation and Human Capital Committee (“CHCC”) of the Board, the Committee shall oversee management’s efforts to define, communicate and instill the Company’s principles relating to ethics, conduct and employee behavior, including tone from the top. The Committee will receive reports from management, at least annually, on efforts to foster the desired culture and promote ethical behaviors and to encourage employees to escalate issues and share feedback without fear of retaliation. The Committee will oversee the Company’s conduct risk management framework.

And in the 2023 Proxy, the company adds “risk management” as an important issue that is formalized as a performance metric in 2022:

The most important financial performance measures used by the Company to link executive compensation actually paid to the Company’s NEOs, for the most recently completed fiscal year, to the Company’s performance are:

1.Return on Equity ("ROE");

2.Relative TSR (the Company’s TSR as compared to a peer group established by the Compensation and Human Capital Committee);

3.SVB stock price; and

4.Risk Management

In 2022, the Comp/HC Committee adopted a formalized framework for assessing risk taking across four different evaluation areas for all NEOs (including the CEO), including (i) performance against stated risk management goals, (ii) performance against assigned risk-related objectives and key results, (iii) qualitative feedback on risk behaviors from risk partners in the second line of defense and (iv) analysis of any key risk events or deficiencies. (2023 Proxy)

Overall, risk management was repeatedly and explicitly called out when discussing 2022 annual bonus payouts to executives:

CEO: Strong leadership of the continued evolution of risk management and controls throughout the organization

CFO: Strong leadership and support for the Company to meet expectations for large financial institutions ("LFI") and promotion of a strong risk culture

President of Silicon Valley Bank: Engagement on risk management initiatives and priorities and ongoing efforts to instill a strong risk culture

GC: Driving of risk management throughout the Legal function, resolving issues in a timely manner and proactively identifying risks

The importance of risk management is literally beaten over the reader’s head when reviewing the 2023 Proxy, and yet, the company didn’t have a Chief Risk Officer for much of 2022 and the market had little idea how “bad” the situation was (relative to Board efforts) partly due to the non-existent disclosures tied the the Chief Risk Officer’s departure (which would have made risk management a top of mind topic for investors).

Needless to say, it’ll be interesting to see how things play out, but there will certainly be lawyers and regulators involved for some time, and I wouldn’t dismiss clawbacks happening as a result of these decisions and the subsequent FUD that was created.